How Data Center Growth Is Rewriting the Grid Playbook

Artificial intelligence is no longer just a headline driver, it’s a load driver. Hyperscale and colocation campuses tied to AI, cloud, and content delivery are creating step-changes in electricity demand that most utility plans didn’t contemplate even three years ago. Across U.S. ISO/RTOs, long-term load forecasts are being revised up, capacity prices are moving, and interconnection backlogs are reshaping development timelines.

The New Load: Big, Fast, and Clustered

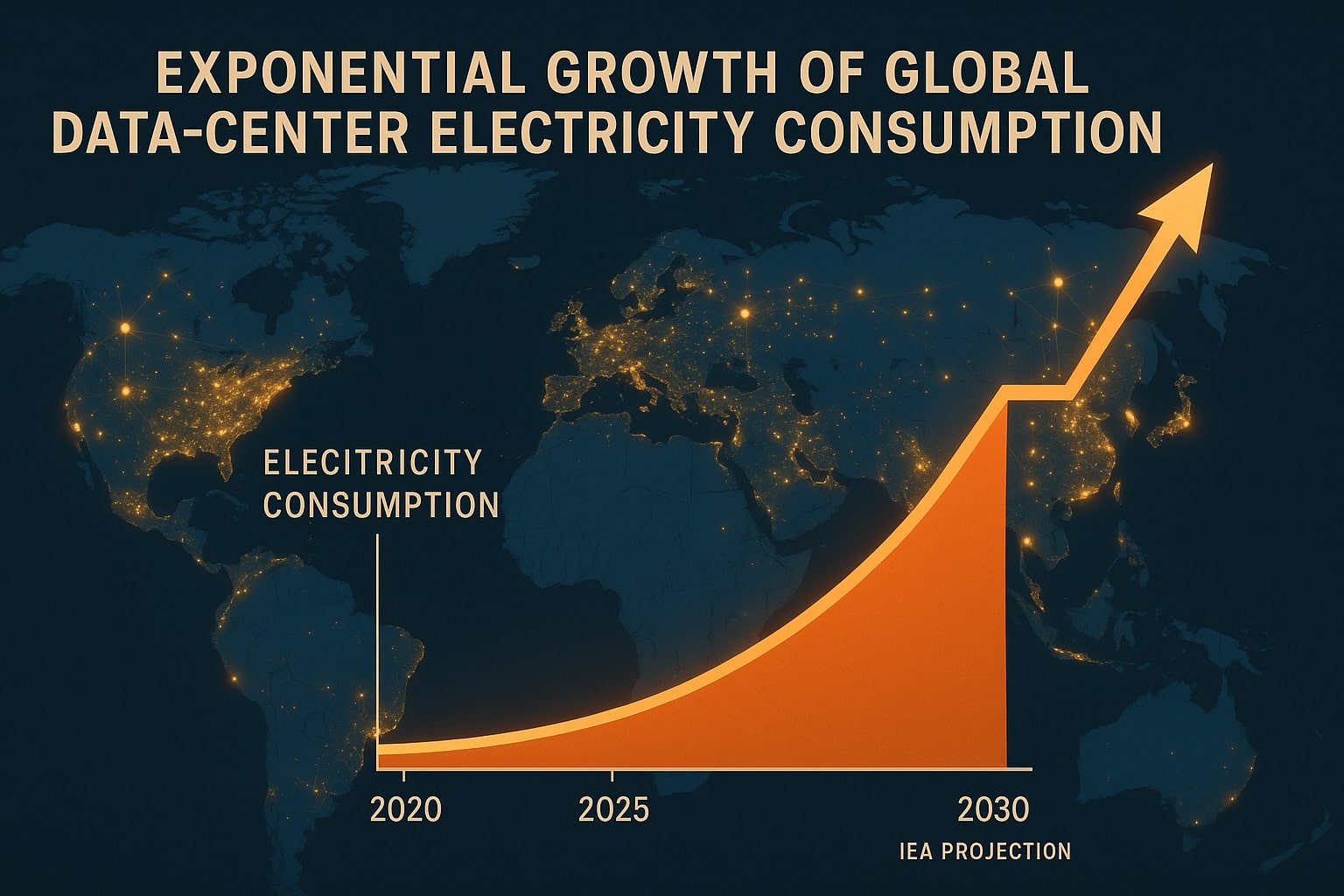

The growth isn’t incremental. The IEA projects global data-center electricity consumption could double by the end of this decade, expanding ~15% per year and approaching ~3% of global demand by 2030. U.S. outlooks echo the trend EIA’s Short-Term Energy Outlook shows record national consumption in 2025–2026 with data centers as a prime contributor. In PJM, the 2025 Load Forecast points to materially higher winter peaks and multi-percentage-point annual growth in some zones.

Two features matter for planners: concentration and simultaneity. Loads are clustering near fiber routes and large substations (Northern Virginia in PJM DOM is the poster case), compressing timelines for 230–500 kV reinforcements and driving a need for advanced thermal ratings, dynamic line ratings, and non-wires options to buy time. Several jurisdictions now assume gigawatt-scale new load blocks within a single planning cycle, far beyond “organic” commercial growth.

Why This Isn’t Yesterday’s Commercial Load

Data centers pose a different operating profile than typical C&I customers:

- High load factor with limited diurnal diversity; when tied to AI training clusters, the duty cycle can be near-continuous.

- Power-quality sensitivity (harmonics, voltage flicker limits, step-load tolerance) that pushes utilities to study protection coordination, short-circuit duties, and dynamic VAR support early.

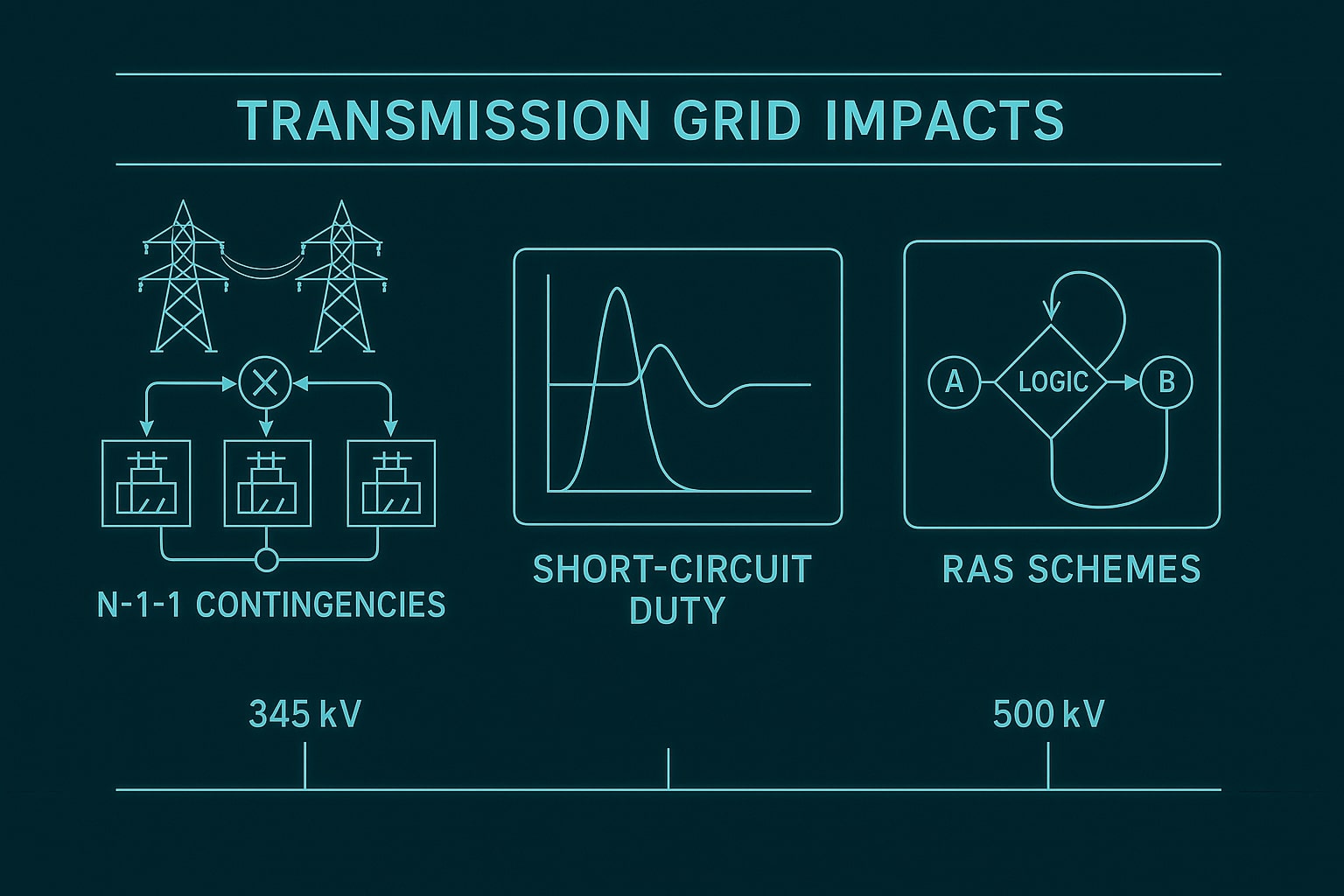

- Location-driven transmission impacts, including upstream N-1-1 contingencies and remedial action schemes (RAS) at the 345 – 500 kV level.

In short: traditional distribution planning with static coincident factors won’t cut it. Utilities are increasingly running full nodal load-flow and stability studies (PSS®E/PSCAD) from the server hall back to the backbone, and evaluating grid-forming inverter options to improve ride-through and system strength.

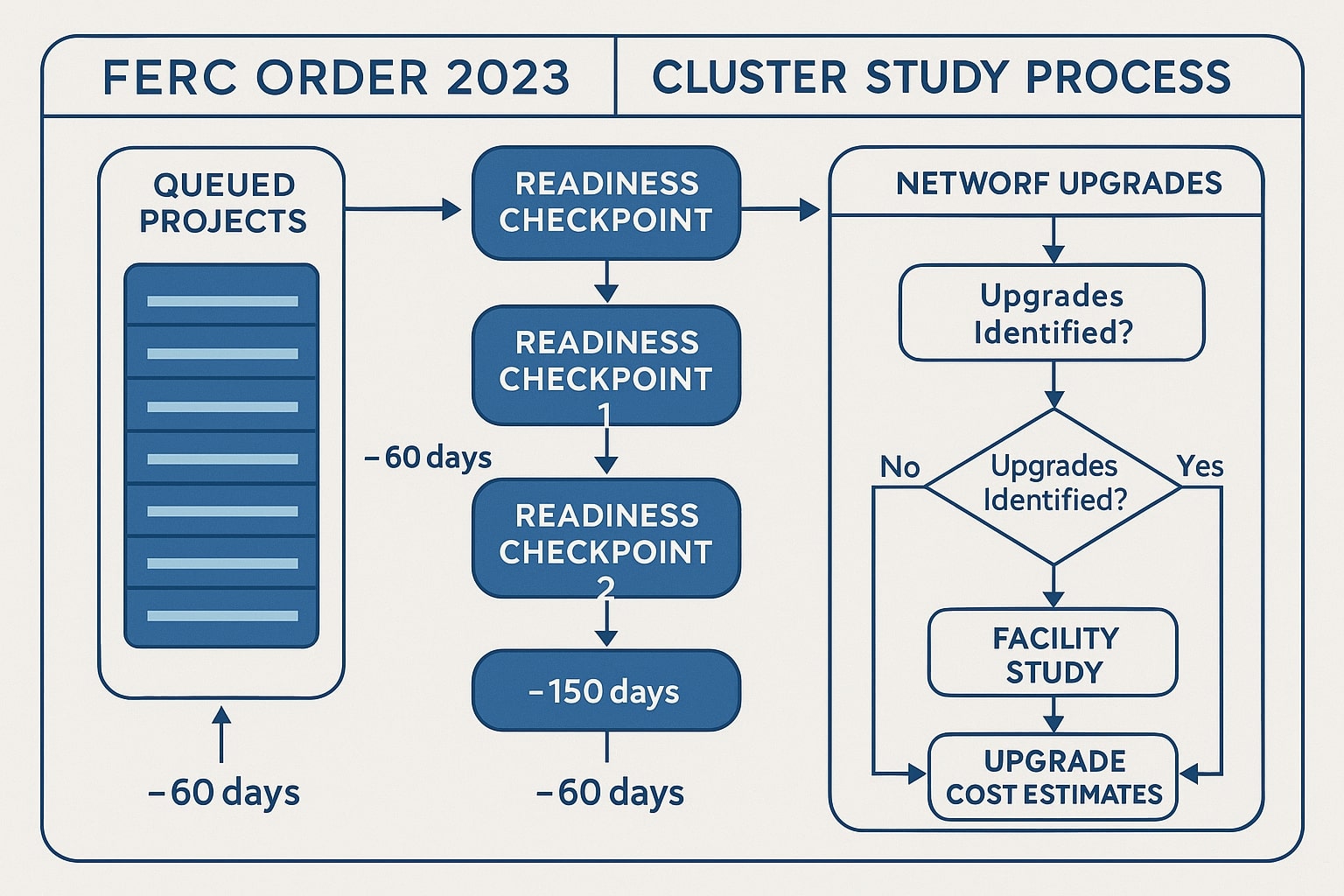

Interconnection Reality: Cluster Studies, Faster…But Not Simple

FERC Order No. 2023 pivoted the industry to clustered interconnection studies, standardized timelines (e.g., ~270 days for cluster studies), and heightened readiness requirements. The goal: clear queues faster and align cost allocation. It helps, but in load-dense pockets, restudies still occur as earlier-queued network upgrades shift, and load additions arrive in parallel with utility-scale renewable and BESS projects competing for the same transmission headroom. Developers should plan for network upgrade risk and pre-screen sites using hosting-capacity and short-circuit headroom maps before filing.

Transmission Expansion Meets the Clock

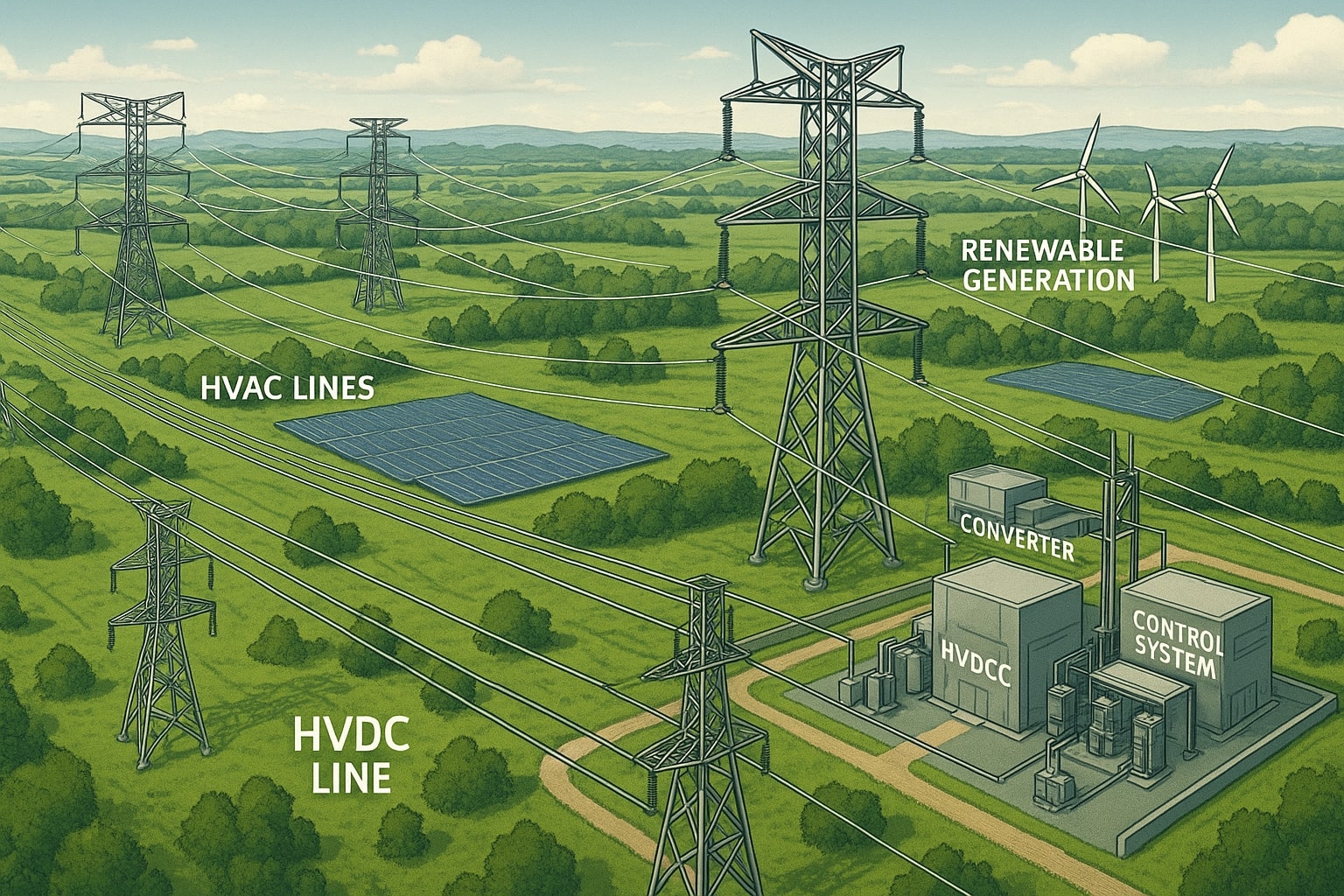

The clean-energy transition already needed transmission; AI-era load makes it urgent. ERCOT, for example, is seeing the fastest demand growth among major U.S. grids and has launched grid-modernization initiatives to keep pace. Nationally, EIA projects record electricity use in the mid-2020s, while several ISOs are revising up peak trajectories. The practical takeaway: proactive corridor planning (including HVDC backbones and controllable ties) moves from “nice to have” to “schedule-critical.” Where new 345–525 kV AC lines are slow to permit, HVDC can unlock long-distance transfers with tighter right-of-way and precise flow control, valuable when balancing large, lumpy loads against variable renewable integration.

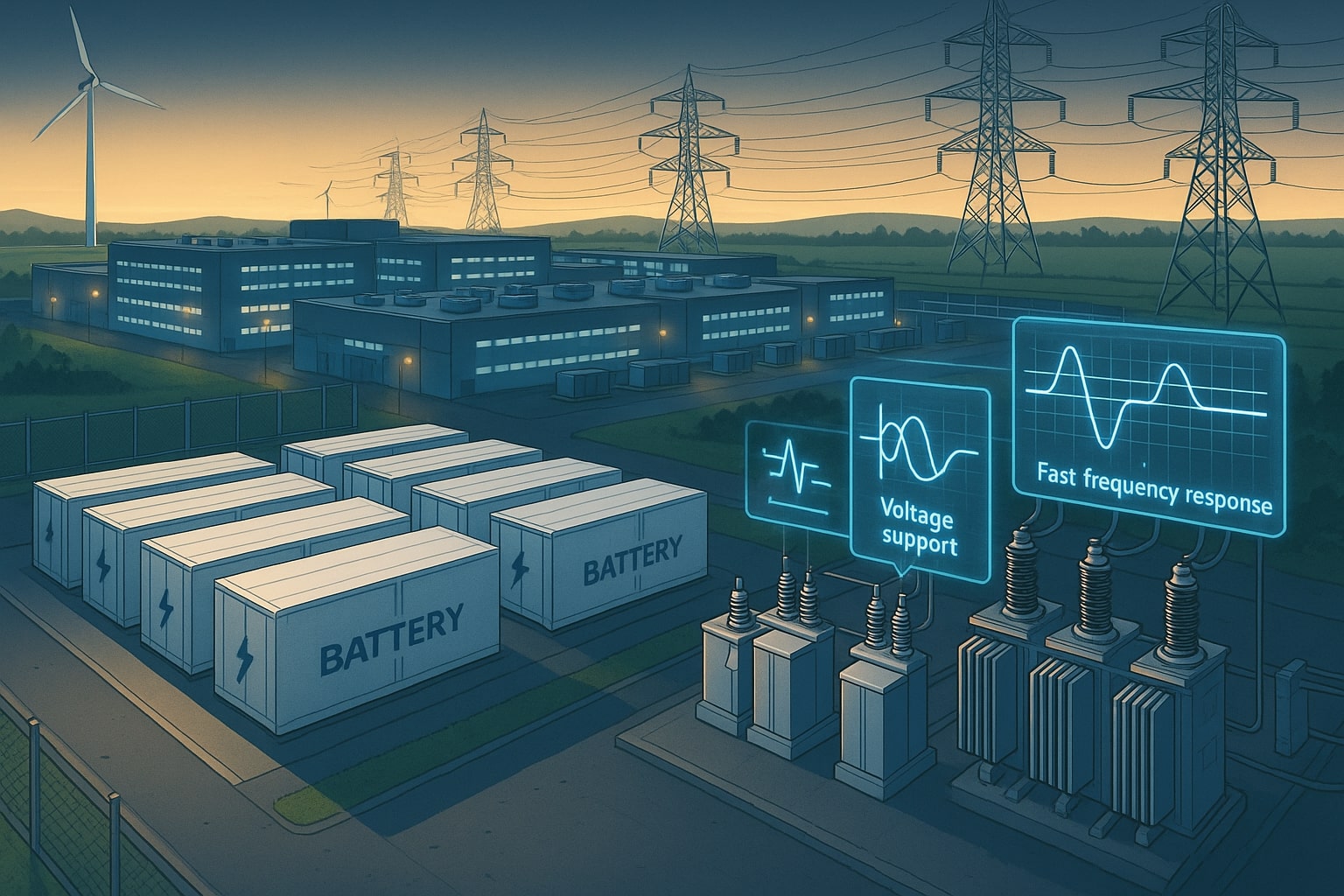

BESS: More Than Arbitrage – A Grid Support Asset

Battery Energy Storage Systems near data-center clusters are graduating from price-spread arbitrage to reliability assets: fast frequency response, voltage support, black-start assistance, and N-1 post-contingency support. Some utilities are now modeling co-located BESS as part of non-wires portfolios to defer transformer banks or 230 kV lines by shaving credible contingencies. Dominion’s 2024 IRP shift from ~100 MW contemplated storage in 2022 to multi-GW by the late 2030s, illustrates how planning assumptions are changing as clustered load rises. Expect more grid-forming BESS requirements baked into interconnection agreements for large load customers, especially where system strength (SCR/ESCR) is marginal.

What “Good” Looks Like: A Practical Playbook

1) Start with the bus, not the parcel.

Screen at the transmission node first: available fault duty, thermal/voltage headroom, transfer limits, and remedial action constraints. Then step down into distribution.

2) Run the right studies early.

Move beyond steady-state power flow. Include short-circuit, protection coordination, dynamic stability (small-/large-signal), EMT where needed, and harmonic assessments. Specify power-quality limits in the point-of-connection (POC) agreement.

3) Design for flexibility.

Mandate on-site or near-site BESS, fast under-frequency response, and ride-through profiles aligned with ISO/RTO PRC standards. Use SVC/STATCOM for dynamic VARs where grid strength is low.

4) Hedge the interconnection path.

Price network upgrades and restudy risk into site selection. Engage early on affected-system coordination (neighboring utilities/ISOs) to avoid surprises late in the cluster.

5) Think portfolio, not project.

Pursue a blend of renewable PPAs, behind-the-meter resources, and HVDC/transfer rights to manage 24/7 carbon goals without straining local feeders. Many operators now maintain a diversified supply stack (utility-scale wind/solar from remote regions + local firming).

6) Modernize operations.

Adopt AI-enhanced load forecasting that treats AI training schedules differently from inference or traditional IT loads. Feed those forecasts into probabilistic planning and capacity accreditation, reflecting performance during extreme weather.

A Candid View on Costs

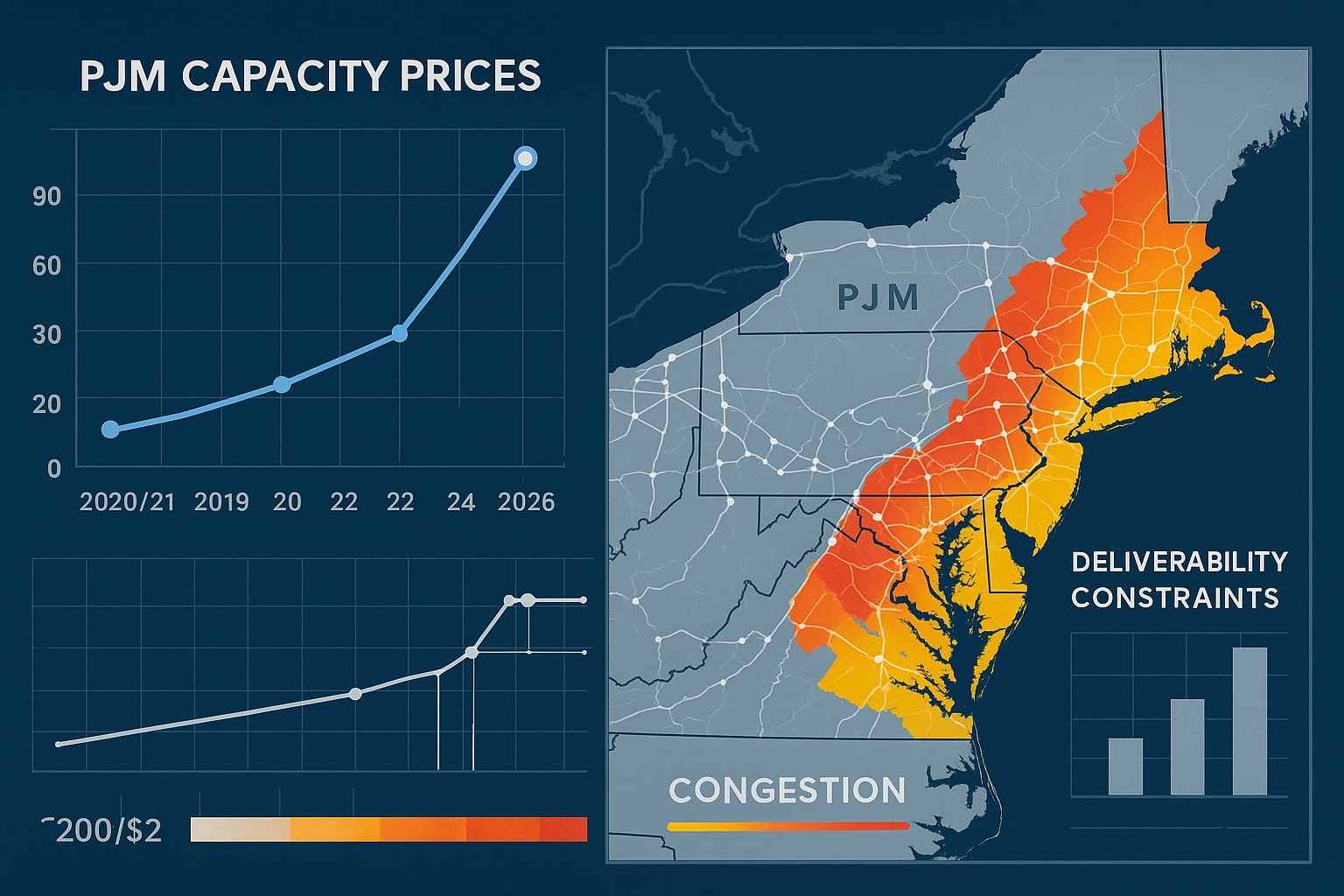

Markets are already pricing the challenge. PJM’s capacity prices jumped sharply for 2026/27 in part due to expected data-center-driven demand, signaling the system value of firm capacity and deliverability. The lesson for executives: the cheapest plan on paper can be the most expensive in congestion and curtailment. Treat deliverability and system strength as first-order value drivers alongside cents/kWh.

Building for the Loads We Actually Have

Data centers are not a future scenario; they’re the present reality. The utilities and developers who win will be the ones who upgrade their playbook, cluster-aware interconnection strategy, HVDC and non-wires optionality, grid-forming resources, and probabilistic planning before the queue dictates it for them. Convert uncertainty into engineered optionality now, and the next decade of digital growth can coexist with renewable integration and grid reliability.

Author: Maryam Asmat

COO

PowerTek Global